Refrigerators and Water Pumps Have Reached a Critical Crossroads: Here’s What the Off-Grid Solar Sector Should Do Next

In this blog, we explore the key differences and similarities between refrigerators and solar water pumps (SWPs)

By Jenny Corry Smith, Senior Manager at CLASP, and Riley Macdonald, Associate at CLASP, Co-Secretariat to Efficiency for Access

This blog is the second in a four-part series featuring key findings from Efficiency for Access’ 2021 Solar Appliance Technology Briefs. This series provides a synthesis of cross-cutting trends for 11 off-grid appropriate appliances, equipment, and enabling technologies, grouped by relative market maturity. Category groupings include near-to-market appliances (TVs and fans), emerging appliances (SWPs and refrigerators), horizon appliances (electric pressure cookers, cold storage, milling equipment, and e-mobility), and enabling technologies (permanent magnet motors, ICT equipment, and interoperability).

In this blog, we explore the key differences and similarities between refrigerators and solar water pumps (SWPs). We’ve categorized these products as “emerging” appliances based on best-available quantitative data (e.g., number of companies in the marketplace, global sales volumes, product performance data, and investment capital) and qualitative data (e.g., stakeholder interviews and on-the-ground learnings). Generally speaking, refrigerators and SWPs do not yet have the market reach of near-to-market appliances (fans and televisions), but they remain further along the market development curve than other technologies, like solar-powered mills, cold storage rooms, and other “horizon” appliances (Figure 1).

We recognize that the categorization in Figure 1 is somewhat subjective and may overly simplify national or regional nuances. For example, from July 2018 — December 2020, SWPs sales in Kenya represented 60% of all reported sales in sub-Saharan Africa. While it’s fair to categorize the Kenyan market for SWPs as emerging, perhaps approaching near-to-market, uneven sales show stark differences across regional and national markets. That said, grouping off-grid appliances by relative maturity can help better characterize the market for similar product classes and identify common next steps to help them move up the market development curve together.

The solar water pump brief focuses on agricultural applications of small-scale solar-powered pumps able to irrigate one to five acres. They can pump water from surface sources such as lakes or streams or from groundwater via a well or borehole. The refrigerator brief covers refrigerators that are intended for domestic and light commercial use, such as beverage cooling. This product category does not encompass agricultural cold storage units, which will be covered in the horizon series this July, nor does it include refrigerators intended for vaccine storage, which are an important but different market segment.

Our data and evidence show SWPs and refrigerators are approaching a critical crossroads. Intelligence and insights on the SWP and off-grid refrigerator ecosystem have improved drastically in recent years. Researchers, donors, and implementing organizations now have a much clearer understanding of these products’ impact on consumers’ livelihoods. Likewise, private sector companies know more about the market potential and how to properly design and sell products. In 2017, only a few companies were designing SWPs for smallholder farmers and we had very little data or research. Today, the Low Energy Inclusive Appliances Program has published market research to fill the knowledge gap, 12 of the 16 members of the Efficiency for Access Donor Coalition fund programs or companies with an SWP focus, and 30 companies participated in the 2019 Global LEAP Awards SWPs competition.

There has also been a significant increase in the number of refrigerator brands available to off-grid consumers. Just five years ago, a handful of off-grid refrigerator brands were active in the market. By 2017, 11 refrigerator manufacturers with 20 products participated in the Global LEAP Awards, and by 2019, 21 manufacturers submitted 39 products for the Awards. This is likely due to the fact that in 2017, most off-grid solar refrigerators were intended for vaccine storage and were too expensive/overdesigned for household and light commercial applications. Now, more manufacturers are optimizing price and performance to target off-grid households and businesses.

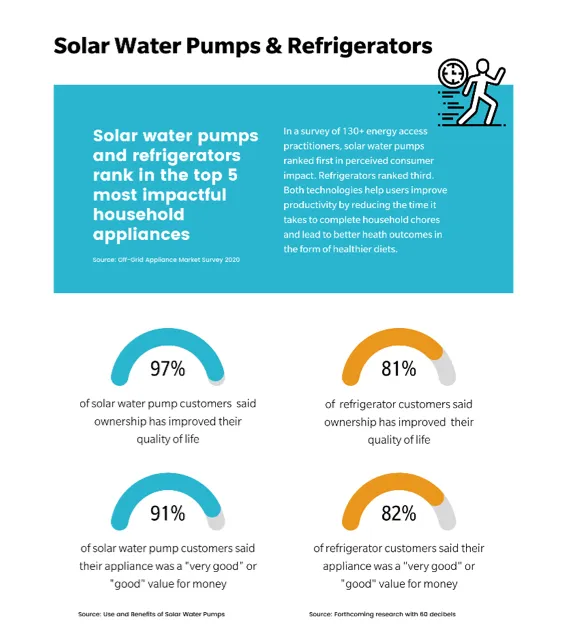

The evidence base has also grown to demonstrate the impact these products can have on off-grid users. One of the most documented and celebrated benefits is increased income. In one unpublished study with refrigerator customers done through the Global LEAP Results-Based Financing mechanism, we found that 87% of customers used their refrigerator in a business and were able to increase their daily incomes by 2.5 times. Another study conducted with M-KOPA customers using the Youmma refrigerator in rural Kenya found that small businesses reported increased weekly income between US$1 to US$40 on average. For SWPs, access to irrigation can increase yields by as much as three-fold, providing households with a more predictable source of income. Farmers also reduce expenditures related to irrigation by up to 91% after purchasing a solar pump.

Beyond the economic benefits, refrigerator consumers have reported better diets, lower stress, increased convenience, and time savings, while SWP users have more confidence in their farming outcomes, improved productivity and resiliency, and increased the amount of land farmed. For both products, users report improvements in quality of life and time savings because of less time spent collecting water and shopping for food. These outcomes can be especially impactful for women — refrigerators and SWPs were both ranked within the top 5 most impactful household appliances for women in the 2020 Off-Grid Appliance Market Survey (Figure 2).

Affordability is a big challenge (perhaps the biggest challenge) to realizing the true social and economic benefits of SWPs and refrigerators. Only 0.5% of smallholder farmers in Sub-Saharan Africa will be able to afford a pump by 2030. Pumps available on the market range in cost from US$600–2,000 — but the average annual income for a smallholder farmer in India is US$1,692. In Africa, only 4% of rural households own a refrigerator. Even with financing available, only 68 million households — roughly 15% of all off- and weak-grid households — could afford an off-grid refrigerator. To help address this gap there needs to be improved access to consumer financing, smart subsidies, R&D funding to spur innovation, and policy reforms to reduce VAT and tariffs for solar-powered appliances — particularly those which can help people improve livelihoods.

Appliances need to be appropriately designed, durable, and of high quality to promote market growth and protect consumers from poor-quality products. Due to their high costs, refrigerators and SWPs are a major investment for most households. A faulty or unreliable product could prove financially disastrous for a family. A key challenge for refrigerator manufacturers is figuring out how to optimize price, efficiency, and performance. We are optimistic that with continued R&D efforts and innovations from product manufacturers, these price and performance improvements will manifest in the market in the next few years. For SWPs, designing products that can withstand variances in water quality, as well as transport in rugged terrain, and are easy to repair and maintain are some of the biggest technical hurdles for manufacturers to overcome. Similar to refrigerators, these issues are best addressed through innovation and R&D.

Quality assurance (QA) is key to enhancing refrigerator and SWPs performance and durability. QA not only ensures that a product delivers its basic service (i.e., cooling or pumping), but also that it’s protected from early failure through a warranty and after-sales care. After-sales care is paramount because, beyond their high price tag, refrigerators and SWPs are technically complex. Many customers are first-time users located in rural areas far from specialized technicians able to fix their product if it breaks. Companies can address this through consumer education on how to use and maintain the products, and also through services like providing remote and local technical support, and ensuring spare parts are available locally.

Finally, partnerships are critical to reaching and empowering end-users to turn products into productive assets. Refrigerators and pumps are large, bulky products, especially when you consider the power system needed to run them. It can be difficult for manufacturers to find distribution partners who can overcome these challenges and reach rural customers. Likewise, distribution specialists can find it challenging to locate equipment manufacturers that sell appropriately designed products at an affordable price. For SWPs, closer partnerships are needed across the agriculture, water, and energy sectors. SWPs will only be transformative if a farmer can make linkages to off-takers and also get advice on how to optimize irrigation alongside the use of other inputs like improved seeds and fertilizer.

For more insights on refrigerators and SWPs, as well as televisions and fans, please see our collection of long-form technology briefs and snapshots. We will continue to launch briefs and snapshots for other technologies throughout the summer. Up next in July are horizon appliances (electric pressure cookers, cold storage, milling equipment, and e-mobility). Please be sure to subscribe to our newsletter to be notified of all new releases.

***

About the 2021 Solar Appliance Technology Brief Series

The 2021 Solar Appliance Technology Briefs synthesise the latest market intelligence and chart the pathway to commercialisation for 11 disruptive technologies, including refrigerators and SWPs. New collections of technology briefs will be released monthly from May 2021 through August 2021, with groupings based on our assessment of their market maturity level. Each release will include a summary blog post, highlighting key similarities and differences across the featured technologies and the interventions needed to scale. Category groupings include near-to-market appliances (TVs and fans), emerging appliances (SWPs and refrigerators), horizon appliances (electric pressure cookers, cold storage, milling equipment, and e-mobility), and enabling technologies (permanent magnet motors, ICT equipment, and interoperability).